PM Jeevan Jyoti Bima Yojana 2025: Life insurance is one of the most important financial tools a family can have — yet for decades, it remained out of reach for India’s poor and lower-middle-class households. Private life insurance policies were expensive, had complex terms, required medicals, and came with heavy paperwork that made them inaccessible to those who needed them most.

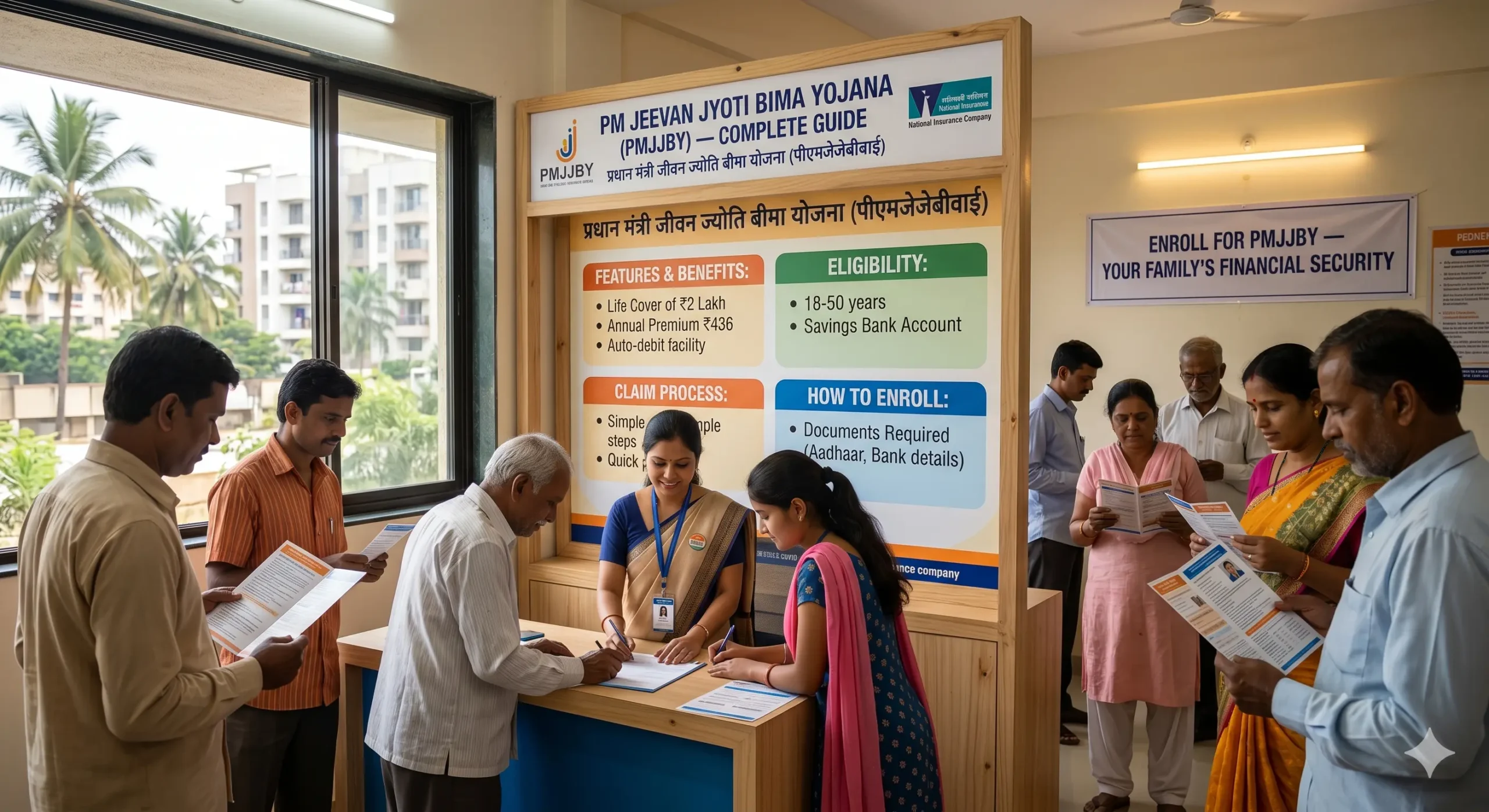

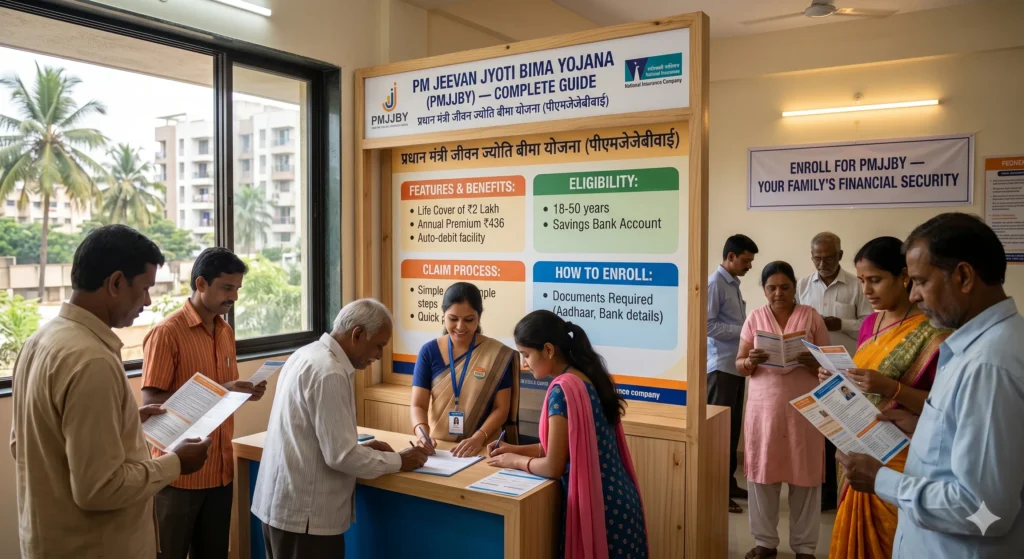

The Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) changed all of that. Part of the Jan Suraksha initiative launched in 2015, PMJJBY provides life insurance cover for death due to any cause, offering ₹2 lakh to the beneficiary’s family in the event of the policyholder’s death, at a premium of just ₹436 annually — approximately ₹1.19 per day.

No medical tests. No complicated paperwork. No agents. Just a simple auto-debit from your bank account every year — and your family is protected.

In May 2025, PMJJBY completed 10 years of providing vital social security to millions of Indians. The Jan Suraksha Schemes — PMJJBY, PMSBY, and Atal Pension Yojana — have completed 10 years of providing vital social security benefits to millions of Indians.

Table of Contents

What Is PM Jeevan Jyoti Bima Yojana?

PMJJBY is a one-year cover term life insurance scheme, renewable from year to year, offering life insurance cover for death due to any cause. ₹2 lakh is payable on a subscriber’s death due to any cause.

It is offered through banks and post offices in partnership with life insurance companies including LIC, ICICI Prudential Life, SBI Life, HDFC Life, and others. Enrolment is done through your bank account — no separate insurance account or agent is needed.

Key Features of PM Jeevan Jyoti Bima Yojana

1. ₹2 Lakh Death Cover for Any Cause

Unlike accident-specific insurance, PMJJBY covers death from any cause — illness, accident, natural death. The nominee receives ₹2 lakh regardless of how the policyholder died.

2. Extremely Low Premium — ₹436/Year

The premium payable is ₹436 per annum per subscriber. This works out to just over ₹1 per day — making it the most affordable life insurance product available to any Indian citizen.

3. Auto-Debit — No Manual Renewal Needed

The premium is automatically deducted from the subscriber’s savings bank account every year, typically between May 25 and May 31. The policy renews automatically unless cancelled — no need to reapply every year.

4. Pro-Rata Premium for Mid-Year Enrolment

For those getting enrolled under PMJJBY for the first time during the middle of the policy period, payment of pro-rata premium is allowed: enrolment in June–August requires the full annual premium of ₹436; enrolment in September–November requires ₹342; enrolment in December–February requires ₹228; and enrolment in March–May requires ₹114.

5. Tax Benefits

Premiums paid are eligible for deduction under Section 80C of the Income Tax Act, further reducing the effective cost for taxpayers.

6. No Medical Examination Required

PMJJBY has no medical test requirement — any eligible bank account holder can enrol regardless of their health condition.

Eligibility Criteria

PMJJBY is available to individual bank or post office account holders aged 18 to 50 years.

Key eligibility points:

- Must be an Indian citizen with a savings bank or post office account

- Age: 18 to 50 years at the time of enrolment

- People who join the scheme before completing 50 years can continue to have risk of life cover up to the age of 55 years, subject to payment of premium

- The bank account must have sufficient balance for the auto-debit of ₹436

- Only one PMJJBY policy is allowed per person. If found with multiple covers, excess premiums will be refunded and cover terminated.

How to Enrol for PM Jeevan Jyoti Bima Yojana

Enrolment is simple and can be done through multiple channels:

Through Your Bank (Offline)

- Visit your bank branch where you hold a savings account

- Fill out the PMJJBY enrolment-cum-auto-debit authorisation form

- Submit with a copy of your Aadhaar card

- The bank will register your consent and set up the annual auto-debit

Through Internet Banking or Mobile Banking

Most banks — SBI, ICICI, HDFC, PNB, Bank of Baroda, and others — allow PMJJBY enrolment directly through their mobile banking apps or internet banking portals:

- Log in to your net banking or mobile app

- Go to “Insurance” or “Government Schemes”

- Select PMJJBY and confirm enrolment

- The ₹436 will be auto-debited immediately

Through Post Offices

Account holders at India Post can also enrol at their nearest post office.

How to Claim PM Jeevan Jyoti Bima Yojana Benefits

In the unfortunate event of the policyholder’s death, the nominee should follow these steps:

- Inform the bank where the PMJJBY policy was enrolled

- Obtain the claim form from the bank or download from the insurer’s website

- Submit the following documents:

- Duly filled claim form

- Death certificate

- Nominee’s Aadhaar card and bank account details

- Discharge receipt (signed by the nominee)

- The bank forwards the claim to the insurance company

- The ₹2 lakh claim amount is credited to the nominee’s bank account, typically within 30 days of claim submission

PM Jeevan Jyoti Bima Yojana vs Private Term Insurance — A Comparison

| Feature | PMJJBY | Private Term Insurance |

|---|---|---|

| Annual premium | ₹436 | ₹5,000 – ₹20,000+ |

| Cover amount | ₹2 lakh | ₹25 lakh – ₹1 crore+ |

| Medical test | Not required | Usually required |

| Age limit | 18–55 years | 18–65 years |

| Tax benefit | Section 80C | Section 80C |

| Best for | Low-income households | Middle/high-income households |

PMJJBY is not a replacement for comprehensive term insurance — but for India’s low-income population, it is a crucial, affordable first layer of life protection.

Impact of PM Jeevan Jyoti Bima Yojana in 10 Years

Since its launch in May 2015, PMJJBY has:

- Enrolled over 20 crore subscribers across India

- Paid out thousands of crores in death claims to bereaved families

- Brought life insurance into the lives of the uninsured for the first time

- Worked alongside PMSBY and Atal Pension Yojana to create a three-pillar social security system for the informal sector

- The government’s ongoing saturation campaign (July–September 2025) is actively enrolling eligible citizens who are still uncovered

Frequently Asked Questions (FAQs)

Q1. What happens if there is insufficient balance in my account for the auto-debit? If the auto-debit fails due to insufficient balance, the policy will lapse. You can re-enrol, but there may be a waiting period before full coverage resumes.

Q2. Is the ₹2 lakh cover per year or lifetime? The ₹2 lakh is the death benefit — paid once to the nominee when the policyholder dies. It is not an annual accumulation.

Q3. Can I have PMJJBY and a private term plan simultaneously? Yes. There is no restriction on combining PMJJBY with other life insurance policies.

Q4. Who are eligible nominees under PMJJBY? Any family member — spouse, children, or parents — can be nominated. The nominee must have a bank account for receiving the claim amount.

Q5. Does PMJJBY cover suicide? The policy covers death from any cause. However, specific exclusions (if any) should be verified with the enrolment bank or insurer.

Q6. What is the official portal for PMJJBY? Visit jansuraksha.gov.in or the Department of Financial Services website at financialservices.gov.in.

Conclusion

The Pradhan Mantri Jeevan Jyoti Bima Yojana is proof that life insurance does not have to be expensive to be meaningful. At just ₹436 per year — the cost of a single meal at a restaurant — it gives millions of Indian families the assurance that even if the breadwinner is no longer there, the family will receive ₹2 lakh to help them get back on their feet. If you have a savings bank account and are between the ages of 18 and 55, there is no reason not to be enrolled in PMJJBY. Visit your bank today, enable the auto-debit, and secure your family’s future for less than ₹2 a day.

Rohanshi Mhatre aims to bridge the gap between government initiatives and citizens by delivering clear, reliable, and easy-to-follow information so that everyone can take advantage of available schemes.