Growing old without financial security is one of the deepest fears shared by working-class Indians. Millions of laborers, farmers, domestic workers, street vendors, and daily wage earners spend their entire working lives without access to any formal pension. When their working days are over, they are left entirely dependent on their children or charity—with no guaranteed income of their own.

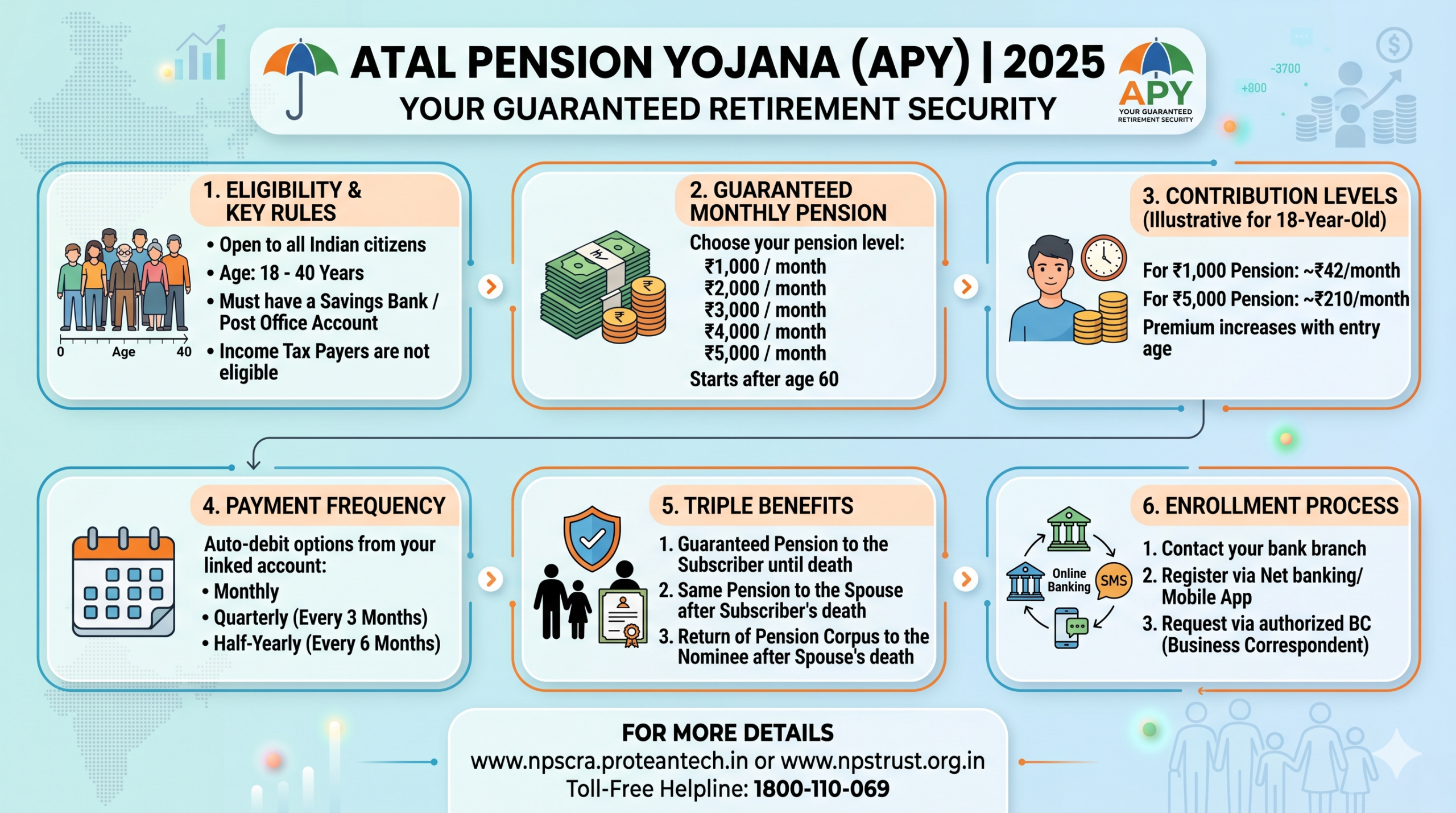

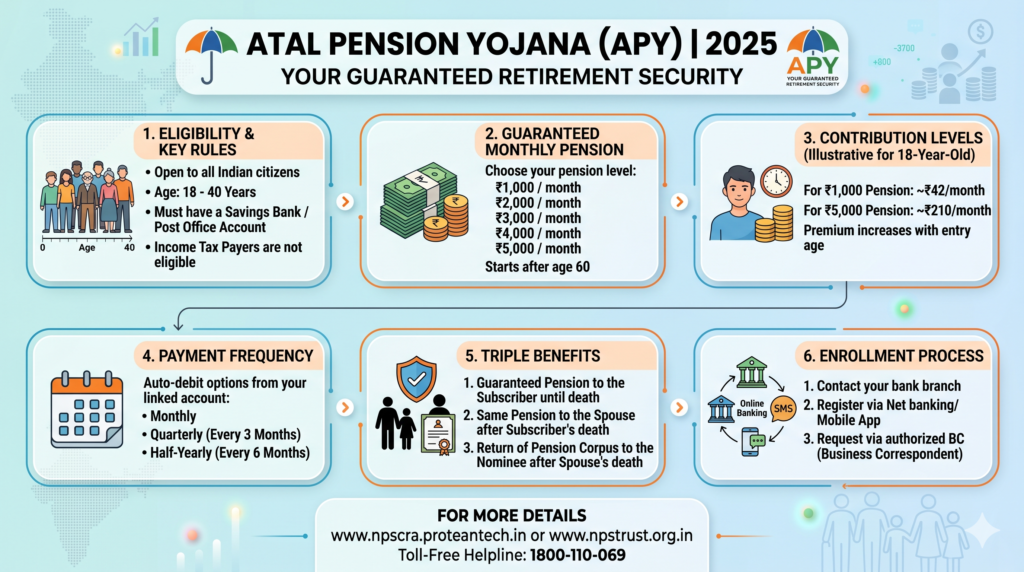

The Atal Pension Yojana (APY) was designed to change that reality. Launched on June 1, 2015, APY is India’s largest pension scheme for the unorganized sector—providing a guaranteed monthly pension of ₹1,000 to ₹5,000 to every subscriber after the age of 60, funded by small, regular contributions made during their working years.

As of April 2026, APY has crossed 9 crore total gross enrollments, with FY 2025–26 becoming the highest-ever year for new additions, with over 1.35 crore new subscribers joining in a single financial year. PFRDA describes APY as a ‘Sampurna Suraksha Kavach’—a Complete Security Shield—because it gives a guaranteed monthly pension to the subscriber, a pension for the spouse on the subscriber’s death, and returns the entire corpus to the nominee after both pass away. ICICI PrudentialICICI Prudential

Table of Contents

What Is Atal Pension Yojana?

Atal Pension Yojana (APY) is a government-run pension scheme open to all citizens of India, mainly focusing on the unorganized sector. APY is administered by the Pension Fund Regulatory and Development Authority (PFRDA) under the National Pension System (NPS). Department of Financial Services

The concept is simple: you contribute a small, fixed amount every month (or quarter or half-year) during your working years, and from age 60 onwards, you receive a guaranteed pension for life. The earlier you join, the lower the monthly contribution required.

Key Benefits of Atal Pension Yojana

1. Guaranteed Monthly Pension

Under the Atal Pension Yojana, a minimum monthly pension between ₹1,000 and ₹5,000 is guaranteed for the beneficiaries. Subscribers can opt for a monthly pension of ₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000, which will start after the age of 60. Department of Financial Services

2. Pension Continues for Spouse

After the subscriber’s demise, the spouse will continue to receive the same pension amount until their death. This means the household pension income continues uninterrupted even after the primary subscriber passes away. Sudlife

3. Corpus Returned to Nominee

After the demise of both the subscriber and the spouse, the nominee will receive the accumulated corpus. This means APY is not just a pension plan but also a wealth transfer tool—the entire accumulated fund is returned to the family even after both members are gone. Sudlife

4. Affordable Contributions

An 18-year-old subscriber contributes between ₹42 and ₹210 per month for a pension of ₹1,000 to ₹5,000. A 40-year-old needs to contribute between ₹291 and ₹1,454 per month. The earlier you join, the smaller your monthly contribution and the bigger your long-term benefit. ICICI Bank

5. Tax Benefits

Contributions made towards the Atal Pension Yojana are eligible for tax benefits. Individuals can claim a deduction of up to 10% of their gross total income, subject to an overall limit of ₹1.5 lakh. In addition, an extra deduction of up to ₹50,000 is available for contributions made to the scheme. Life Insurance Corporation of India

6. Combined Family Pension Up to ₹10,000/Month

Atal Pension Yojana can help a husband and wife plan a combined pension of around ₹10,000 per month by keeping two separate APY accounts and paying as per the chart. A couple can each hold an APY account and each receive ₹5,000/month—creating a joint monthly income of ₹10,000 in retirement. ICICI Prudential

Eligibility Criteria

- Must be an Indian citizen aged 18 to 40 years at the time of joining

- Must have a savings bank account or post office savings account

- Must not be an income tax payer (from October 2022 onwards, income taxpayers are not eligible for APY)

- Must not be a member of any other statutory social security scheme (EPF, EPS, ESIC members are excluded)

APY Contribution Chart (Sample)

The monthly contribution varies based on your age at joining and the pension amount you choose:

| Age at Joining | ₹1,000/month pension | ₹3,000/month pension | ₹5,000/month pension |

|---|---|---|---|

| 18 years | ₹42/month | ₹126/month | ₹210/month |

| 25 years | ₹76/month | ₹226/month | ₹376/month |

| 30 years | ₹116/month | ₹347/month | ₹577/month |

| 35 years | ₹181/month | ₹543/month | ₹902/month |

| 40 years | ₹291/month | ₹873/month | ₹1,454/month |

The clear lesson: join as early as possible. An 18-year-old pays only ₹210/month for a ₹5,000/month pension for life — while a 40-year-old must pay ₹1,454/month for the same pension.

How to Join Atal Pension Yojana

Method 1: Through Your Bank (Offline)

- Visit your bank branch with your Aadhaar card and mobile number

- Fill the APY Registration Form (updated form mandatory from October 1, 2025)

- Choose your pension amount (₹1,000 to ₹5,000) and contribution frequency (monthly/quarterly/half-yearly)

- Provide nominee details

- The bank will activate your APY account and set up the auto-debit

Method 2: Online via eNPS Portal

Visit the eNPS NSDL portal at enps.nps-proteantech.in. Select Atal Pension Yojana → APY Registration. Fill in details and complete KYC via Aadhaar XML/OTP/Virtual ID. Decide on your pension amount and contribution frequency. Enter nominee details and complete e-Sign via Aadhaar OTP. Sudlife

Method 3: Through Net Banking or Mobile Banking App

Most banks—SBI, PNB, Canara Bank, Bank of Baroda, ICICI, HDFC, and Axis—offer APY enrollment directly through their internet banking or mobile banking apps under the “Government Schemes” or “Pension” section.

New APY Form — Updated from October 1, 2025

From October 1, 2025, new subscriber registration is accepted only on the revised APY form issued in line with PFRDA guidelines. Post offices and banks have been told to display the new rules and take applications only on the updated form with FATCA/CRS declaration. ICICI Prudential

The FATCA/CRS declaration requires applicants to confirm if they have any foreign tax residency. This update is part of global financial compliance requirements and does not change the scheme’s benefits or contribution structure. ICICI Bank

How to Check Your APY Account and Contribution Status

Subscribers can check their APY account balance and contribution history through the following:

- The NPS/APY mobile app by PFRDA

- The eNPS portal at enps.nps-proteantech.in

- Their bank’s mobile banking app under the APY section

- By calling their bank branch

Premature Exit from APY

Withdrawal from APY is generally not permitted before the age of 60. However, early exit is allowed in exceptional cases such as terminal illness. If the contributor dies before attaining 60 years of age, the spouse has the option to exit the scheme and claim the accumulated corpus. Life Insurance Corporation of India

This protects the long-term retirement savings objective of the scheme while providing flexibility in genuine emergencies.

Impact of APY in 10 Years

APY has fundamentally changed retirement planning for India’s informal sector:

- FY 2025–26 saw over 1.35 crore new subscribers joining—the highest-ever addition in a single year, driven by rising financial awareness in rural and semi-urban India and coordinated outreach by banks, RRBs, small finance banks, and post offices. ICICI Prudential

- Millions of workers who previously had zero retirement savings now have a guaranteed pension waiting for them at 60

- The spouse pension and corpus return to nominee features make APY one of the most family-friendly pension products in any country

- APY has been instrumental in creating a pension culture among India’s vast informal workforce

Frequently Asked Questions (FAQs)

Q1. Can I increase my pension amount after joining APY?

Yes. You can upgrade or downgrade your pension slab once a year during April.

Q2. What happens if I miss a contribution payment?

A penalty of ₹1 per month for every ₹100 of contribution is charged for delayed payments. If the account is inactive for an extended period, it may be frozen or closed.

Q3. Can a government employee join APY?

Government employees who are already covered by other statutory pension schemes (NPS/EPS) are not eligible. However, contract workers and casual government staff not covered by a statutory scheme may be eligible.

Q4. Is APY available for NRIs?

No. APY is only available to Indian citizens who are residents of India.

Q5. What is the official website for APY?

npscra.nsdl.co.in and jansuraksha.gov.in

Q6. Can a housewife with a savings account join APY?

Yes — any Indian citizen aged 18–40 with a savings account who is not an income taxpayer can join, including homemakers.

Conclusion

The Atal Pension Yojana is India’s most powerful tool for retirement security in the unorganised sector. By requiring only small, regular contributions during working years and guaranteeing a lifelong monthly pension from age 60 — along with spouse pension and corpus return to nominees — APY delivers remarkable value for every rupee contributed. With 9 crore subscribers and FY2025–26 being the scheme’s most successful year ever, APY is clearly resonating with India’s workforce. If you are between 18 and 40 years old, not an income taxpayer, and don’t yet have a pension plan, there is no better time to join APY. Walk into your bank today, fill the new form, and start building your retirement security—one small contribution at a time.

Rohanshi Mhatre aims to bridge the gap between government initiatives and citizens by delivering clear, reliable, and easy-to-follow information so that everyone can take advantage of available schemes.